Why Yield isn’t Money

The Stablecoin Revolution : Part I, The Prohibition on Yield

Hundreds of billions of risk-free dollars a year are leaked from households to banks. This isn’t done by mistake, it’s a critical part of monetary policy.

In this post, I’ll explore the connection between the Narrow Bank Inc., its impact on the potency of monetary policy, and why the GENIUS act prohibits the pass through of yield to stablecoin holders.

The Narrow Bank Inc.

The Federal Reserve rarely refuses a Master Account (i.e., the ability to earn the Fed’s IORB) to a qualified institution. One particularly relevant exception of this was The Narrow Bank Inc.

The Narrow Bank Inc. planned to take no risk on behalf of depositors by parking all funds in a Fed Master Account to earn the Interest Rate on Bank Reserves (IORB Rate). The absence of risk was quite exciting to critics of risky banking practices.

At first glance, The Narrow Bank Inc. sounds great to regulators. A low risk alternative that avoids the moral hazard that looms over banks today. Their target market might be risk-averse depositors - people who are distrustful of banks’ risk management practices and would prefer to opt-in to a risk-free alternative.

But if The Narrow Bank avoids socializing risks and appeals to risk-averse depositors, why would the Fed deny it access ?

To understand the Fed’s motivation, we first need to understand the mechanisms by which the Federal Reserve pays interest on reserves.

IORB and ON RRP

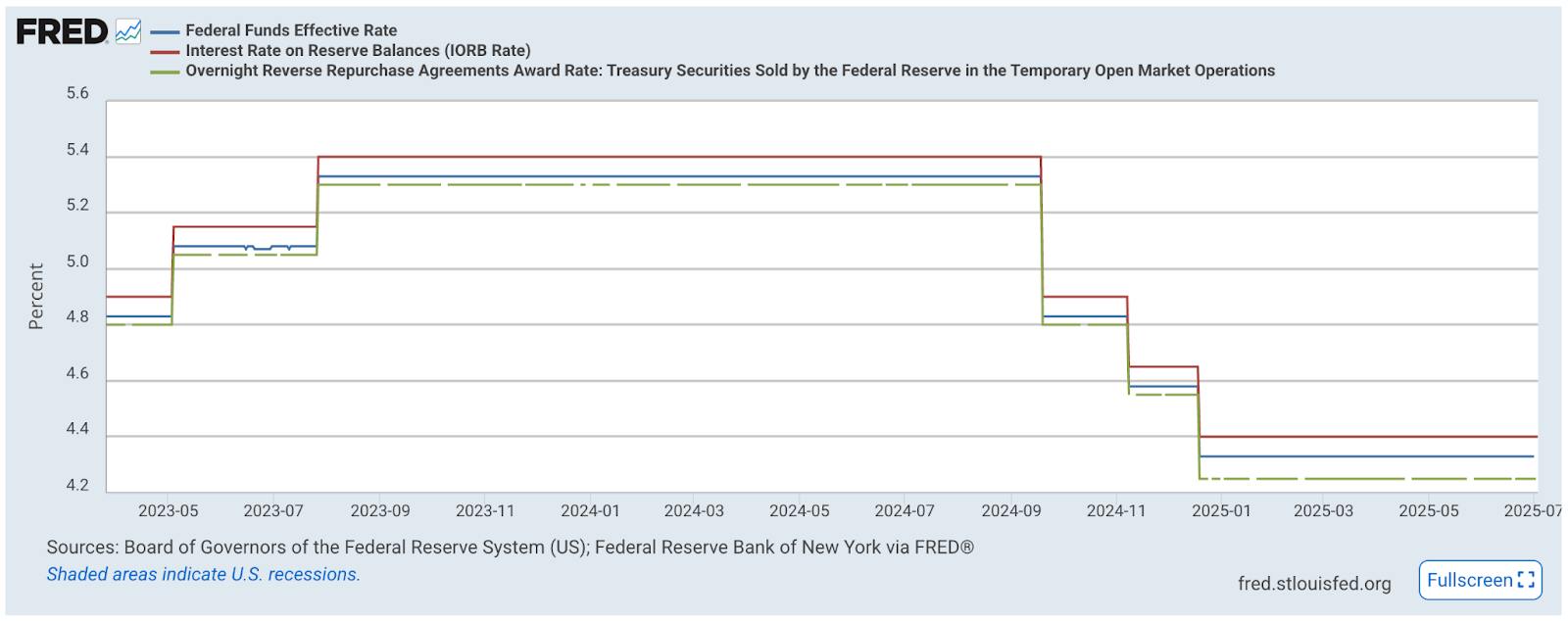

When banks hold reserves with the Fed, they earn a risk and duration free rate IORB rate which currently sits at 4.4%1.

Not all institutions are afforded the same luxury e.g., Money Market Funds (MMFs) and Government Sponsored Enterprises (GSEs). Instead of having access to the IORB rate, these parties can only access the less attractive Overnight Reverse Repurchase Agreements Rewards Rate (ON RRP rate) made available by the Fed. Notably the ON RRP rate is 4.25%2, which is 15bps lower than the IORB rate.

The spread between IORB and ON RRP is not a coincidence - it’s a tool of the Fed’s to enact monetary policy. By maintaining the spread, funds are encouraged to be held within the banking system. If MMFs could earn the safe IORB rate outflows from banks into higher yielding MMFs should follow. Keeping reserves within the banking system is seen as critical for ensuring transactions can be settled.

It also helps the Fed monitor liquidity within the banking system. The corridor helps maintain a private market for overnight loans. MMFs which can’t earn the IORB rate will lend overnight at the Federal Funds Effective rate (EFFR). Since an arbitrage exists for banks which can borrow at the EFFR and earn at the IORB rate, the EFFR typically sits between the ON RRP rate and the IORB rate. This establishes a sort of “thermostat”. If the EFFR gets close to or even exceeds the IORB, it signals to the Fed that banks are starting to borrow significantly from private markets to meet their liquidity needs. In the absence of the corridor, this signal would disappear.

The Narrow Bank Inc. (Actually)

The business model of The Narrow Bank was never to serve risk-averse individuals. Most individuals, regardless of risk aversion, have accounts well below the $250k FDIC insurance cap anyways. So risk-free practices wouldn’t reduce their risk (although greater pass through would improve their returns). As a consequence, moving to a bank with greater pass through rates wouldn’t be particularly attractive until all of the other conveniences of holding money at larger banks are smoothed over.

The Narrow Bank wasn’t oblivious to this. Their real target customer was never end consumers, but MMFs and other institutions that aren’t eligible to earn the risk and duration free IORB rate. These institutions care less about the conveniences banks provide to end customers, and much more about the bps of yield they give up from their inability to park idle reserves with no risk at the IORB rate, which is meaningfully higher than the ON RRP rate they have access to.

If this practice were widespread, it would jeopardize the usefulness of the corridor established by the Fed. Funds would be more likely to move into MMFs. And the EFFR would also cease to be a useful signal on liquidity needs in the banking system, as its new floor would be the IORB Rate.

It would also mean less pressure on MMFs to manage portfolios themselves. Instead of using their funds to buy (and price) assets with duration and credit risks, they would be holding it at the Fed. Major outflows from the U.S. Treasury market (and into the IORB) would cause interest rates on debt of any duration to spike. This would carry major second order effects across the entire economy.

Consumer Focused Narrow Banks and Stablecoins

The Narrow Bank Inc. story is useful because it resembles the concerns that the Fed would have when dealing with a similar model applied to consumers. The popularization of highly liquid, low-risk, yield bearing dollars would resemble similar concerns to those on The Narrow Bank Inc. But whereas The Narrow Bank Inc. aimed to conduct “arbitrage” on behalf of MMFs, the analogous version would allow consumers to “arbitrage” the system too.

The IORB rate is in essence a subsidy for banks that keeps liquidity within their reins. And while MMFs lose on the difference between the IORB rate (4.4%) and the ON RRP rate (4.25%), the average consumer loses orders of magnitudes more from the difference between the average rate passed through to the trillions of dollars in checking deposits (.07%) and the IORB rate.

There is evidence this is already a strong consideration within the new wave of stablecoin regulation. After years of sitting in purgatory, the current presidential administration has been pushing for regulatory clarity. The most relevant example has been the GENIUS act, which just passed in the House with a 68-30 vote, signaling the dawn of a new age of (bipartisan?) crypto regulation.

The relevant clause of the GENIUS act for our purposes is its explicit prohibition on passing through yield.

“(11) PROHIBITION ON INTEREST.—No permitted payment stablecoin issuer or foreign payment stablecoin issuer shall pay the holder of any payment stablecoin any form of interest or yield (whether in cash, tokens, or other consideration) solely in connection with the holding, use, or retention of such payment stablecoin.”

In a sense, stablecoins are prohibited from becoming a consumer version of the Narrow Bank Inc. Notably, the clause does not mention restrictions on the after-market for use cases. There are still various ways in which stablecoins can be used (and are used) to earn around the risk free rate with deep liquidity and no account at the Fed (e.g., over-collateralized lending). If these applications can sufficiently reduce their risk, consumer-oriented constructions still seem within the realm of plausibility. However without access to a Fed Master Account and FDIC insurance for stablecoin holders, it’s unlikely most consumers will rush in given the lower risk-adjusted returns.

Looking Forward

If the IORB rate was passed through to consumers at scale, it would have an even larger impact on the potency of monetary policy than The Narrow Bank Inc. The power of monetary policy is in part predicated on the idea that the economy can be nudged one way or another by controlling the money supply and banking liquidity through influencing the opportunity cost of holding money. Raising interest rates should increase the opportunity cost for households and decrease it for bankings, causing the money supply to fall and in turn disinflation. And the opposite should be true of decreasing interest rates.

In a world with yield-bearing money without tradeoffs, monetary policy becomes less potent : changes in rates would cease to have the same effect on the opportunity cost of holding money. The rates would already be baked into the money people hold, and liquidity would flow out of the banks which don’t follow suit.

The Fed’s prohibition on IORB pass through keeps the banking system liquid, and its favorite policy tools potent. But the decision is not without tradeoffs. It represents a wealth transfer away from the public and towards private banks.

All of that said, until there’s a credible alternative it’s tough to pass further judgement.

As of July 18th

As of July 18th

If I understand correctly, the Fed rejected The Narrow Bank because if it had existed, a large share of the money currently used to buy Treasuries would have gone directly to the Fed to earn the IORB rate. Less demand for Treasuries = lower prices = higher interest rates, and that would have disrupted monetary policy. Is that correct